Ethanol production and its co-products in Europe

Carbon dioxide is the most discussed topic in Europe where the environment and global warming is concerned. Bioethanol appears to be the answer in controlling carbon dioxide emissions and producing “environmentally neutral” energy. In the US, maize is the basis for this. In Europe, however, other grains (mainly wheat) are used for biofuel production. In August, Adisseo, in cooperation with Ajinomoto Eurolysine, organised a mini-symposium on the subject in Strasbourg, France.

By Dick Ziggers

The mini-symposium entitled “Biofuel co-products – Towards a nutritional

evaluation of DDGS” was a pre-conference to the 16th European Symposium on

Poultry Nutrition. Two speakers shared their views on the current biofuel market

in Europe, and more specifically the co-products of this industry.

|

The emphasis on biofuels and its compulsory inclusion levels in car fuels has

placed a lot of pressure on the European grain market. Since a large percentage

of cars use biodiesel as a fuel in Europe, there is less emphasis on bioethanol

and more on the popular biodiesel. In this way, the situation is different to

the US where diesel is almost absent in private cars. Biofuels have an expected

impact on the supply and demand of grains, especially this year with poor

growing and harvesting conditions in many parts of the world.

Increased fuel consumption

The fuel market is certainly not a stable market, and consumption continues

to increase. Fossil fuel consumption is estimated to grow 8% between 2004 and

2010, according to Hémeline Macret, market analyst at Tallage (www.tallage.fr),

an independent statistical bureau on grains movements in Europe. Macret

calculated that biofuel consumption in 2010 will consist of 13.6 million tonnes

(Mt) biodiesel and 7.6 Mt bioethanol. This demand is likely to be met through

the development of existing plants, as well as new plants that are being

created.

The level of bioethanol production capacity from realistic factories is

estimated at 7 Mt, which is the base used for estimating grain demand for

biofuels.

Various feedstocks will be used to produce bioethanol in 2010, including

cereals, sugar beet, food and non-feed waste, cellulose, etc. For some plants,

the feedstocks to be used have not yet been determined. “The demand for grain in

bioethanol production will reach 17.8 Mt in 2010/11: 4.6 Mt maize; 8.7 Mt wheat;

1.1 Mt barley; 2 Mt rye; and 1.3 Mt unspecified grains. Above these quantities,

1.6 Mt of grains could be used in projects that have not determined their

feedstock yet,” Macret said.

The analysts at Tallage expect no big changes in demand from the milling

industry. Following the closure of a maize starching plant in the UK in

mid-2007, maize demand will be 350,000 tonnes less in 2007/08. On the other

hand, a wheat starching plant will open in Manchester, UK, and is to process

750,000 tonnes of wheat from the end of the current crop year. In the malting

industry, a 200,000 tonne reduction in barley usage is expected up to

2010.

Slow rise in animal feed demand

The animal feed industry is also a large consumer of grains and oilseeds.

Macret expects animal feed production in the EU to rise moderately between 2006

and 2010. Production of industrial compound feed for cattle, poultry and pigs

should reach 136 Mt, which is 2 Mt more than current production. It is expected

that on-farm feed will also increase because of slightly higher animal herds and

higher grain availability. The increase in cereal usage by animals is not likely

to materialise since cereals will be faced with growing competition from rape

meal (biodiesel production from rape seed) and grain DDGS. Tallage assumes that

the supply of grain DDGS will reach about 6 Mt in 2010 and the additional supply

of rape meal will reach 12 Mt in 2010. A part of these products will replace

cereals in animal diets.

Figure 1

Figure 1 gives a breakdown of the

expected 6 Mt DDGS production for 2010. Primary DDGS production will come from

wheat, except in Hungary where maize is the basis for bioethanol, and Spain

where barley is used. Total demand for wheat will increase 17% from 106 Mt in

2007/08 to 124 Mt in 2010/11. In the same period, maize demand is expected to

increase by 10% from 60 Mt to 66 Mt, and barley demand to rise 10% from 53 Mt

this season to 59 Mt in three years time. Increases in demand are expected to be

covered by increases in production through higher production per hectare, as

well as the ending of the set-aside policy, which brings a lot of hectares back

to commercial production.

Production processes

Compared to world production of 36 Mt of bioethanol, the current 1.9 Mt

(2005) produced in Europe hardly has an impact on a global scale. However, this

volume is to increase to 8.2 Mt in 2008, according to Christian Delporte,

technical director of starch specialist Roquette (www.roquette.com), France. To

produce one tonne of bioethanol from wheat, 3.3 tonnes of the grain are needed.

In Europe, an area of 0.4 ha is needed (at 8.25 tonnes/ha) to produce that

amount, Delporte explains. The conversion to bioethanol also generates CO2 and

1.15 tonnes of wheat DDGS. However, there are many options to make bioethanol

from wheat. Delporte describes three main processes:

• Process 1 is the simplest process. Wheat is ground, hydrolysed, fermented

and distilled. Before distillation the liquids are separated from the solids by

centrifugation. The solids consist of distiller’s grains and solubles. After

drying, the product can be pelleted into wheat DDGS pellets.

• Process 2 mills wheat into flour and middlings. Only the flour is

hydrolysed, fermented and distilled. After centrifugation, distiller’s grains

and solubles are left over. Together with the middlings, these can be pelleted

into wheat DDGS pellets, however, with a different nutritional value as the

pellets from Process 1.

• In process 3, wheat follows several stages before hydrolysis; in a starch

plant wheat gluten is separated from the wheat (wet milling), as are the

middlings. The wheat starch and the wheat solubles are then hydrolysed and

fermented. The distiller’s grains, solubles and middlings can be pelleted into

wheat DDGS pellets, but with another nutritional value than in Process 1 and 2,

because the gluten was taken out in the beginning.

|

Table 1

gives an overview of the nutritional content

of DDGS from these three processes. These outcomes show that it is very

important to verify the process from which the DDGS are derived. Protein and

starch content will be key factors for differentiation of DDGS. Amino acid

content and digestibility could be very different according to the process;

think of the impact of protein extraction and different heat treatments, such as

distillation, evaporation and drying. If the DDGS are not pelleted it will be

fed in a wet form. This is suitable for cattle and pigs, but not possible for

poultry.

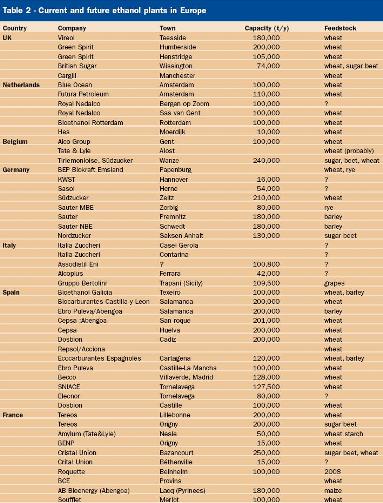

Delporte also showed an interesting overview of current and future ethanol

plants in the main countries of Europe. Table 2 gives an overview.

Source: Feed Tech Vol.

11 nr. 8

Join 26,000+ subscribers

Subscribe to our newsletter to stay updated about all the need-to-know content in the feed sector, three times a week.