Feed scares; how to prepare for the unexpected?

The feed sector has gone through some serious scares lately; from dioxin to melamine and from salmonella to aflatoxins. These scares not only cost money, they also damage the image of the sector. What can be done to prevent it? Feed Tech has put this question to Wilco de Haan, Director Liability at Marsh, eminent insurance broker and risk management consultant. By Emmy Koeleman

them coming.

of dog and cat food in North America recalls 60 million containers of wet food

after it received reports of pets suffering kidney failure. Almost a year after

the event the facts have come to the surface, wheat gluten contaminated with

melamine from China ended up in the pet food and caused disastrous effects.

Thousands of pets died, US$55 million dollars in damage, class action lawsuits,

lost clients and a ruined image. In Europe, we faced several serious dioxin

crises in 2006, after the cancer-causing chemical was detected in pig and

poultry feed used by hundreds of farms.

A similar crisis

happened in Belgium in 1999, in which the industry lost millions of Euro, either

through quarantine of 200 Belgian farms, or through the loss of their export

markets after some countries imposed bans. It turned out that two filters at

Tessenderlo Chemicals were defective, resulting in untreated hydrochloric acid

being delivered to its subsidiary, PB Gelatins. PB Gelatins in turn, supplied

animal feed producers with dioxin contaminated ingredients. These two examples

of feed scares have different backgrounds and consequences. They do however have

one important thing in common, it all started with only one contaminated

ingredient.

A good risk

management plan combined with a good insurance can help to prevent or minimise

the damage after feed contamination or product recall, explains Wilco de Haan

from Marsh. Marsh is part of MMC (Marsh & McLennon Companies) and is expert

in providing advice and solutions in risk strategy and human capital. The

company helps its clients to identify, plan for and respond to critical business

issues and risks. This is important because risks are present in all types of

business. Newspapers and websites often publish advertisements that certain food

products, toys, electrics, clothing and mattresses are recalled.

Empty shelves in a US supermarket. The recalled pet food by

Menu Foods has cost the company millions of dollars.

“However, not all risks have the same impact,” says de

Haan. Feed companies seem to require some extra attention in this. This is

because the animal feed is part of the food chain, which is is a long and

complicated one, marked with many different suppliers and buyers from around the

world. This may sometimes lead to miscommunication with different approaches and

thoughts about quality and safety issues. Secondly, because the end product is

food for humans there is inevitably more scrutiny as it is such a sensitive

area. Animal feed that is used for the production of animal products therefore

need to be of top quality and absolutely safe. In addition, legislation

concerning the production of feed is getting stricter (for example lower maximum

levels for PCBs and mycotoxins). Also supermarkets, due to their oligopolistic

market position, are major stakeholders in this market and sometimes demand

certain quality and certifications for animal feed.

Because

the rules are getting stricter and the potential implications resulting from a

major feed scare become bigger, feed companies are increasingly looking for ways

to offset their risk. “Besides a property damage and business interruption

insurance, a public and product liability insurance, a feed company can nowadays

buy coverage for all the costs associated with product contamination”, explains

de Haan. Such a safety net allows the company to recover defined costs involved

in the recall, as well as insuring that the company has the resources to get

outside assistance.

A special

product contamination insurance is already quite common in the human food

sector. “However, feed companies sometimes don’t need or want such an

insurance,” says de Haan. Many potential risks in the feed industry are already

minimised by simple quality and hygiene procedures (on farm hygiene measures and

joint programmes such as GMP+, HACCP and ISO). If a feed company agreed that

ingredients need to be GMP+ certified, and it turns out not to be the case, the

company can claim the potential damage from the supplier. These measures are all

implemented to prevent risks and claims from other companies in the feed chain.

This is the reason why an increased number of feed companies have adopted GMP+

for example and more local initiatives pop up regarding food and feed

quality.

Quality and

hygiene programmes are very important; however there are still scenarios where

these programmes and measures are not adequate. Menu Foods could not conceivably

foresee that buying the contaminated wheat gluten from China would have such

dramatic consequences. De Haan: “This is where we as insurance broker and risk

management consultant come in. By carrying out an extensive risk inventory, we

gain a better insight regarding what the specific risks are and how these can be

prevented”. A risk management consultant tries to compile a good risk inventory

by asking the following questions:

–

What are the current quality measures at company level?

– Which specific

risks is the primary producer exposed to?

– Where are the measurement points

within the feed/ food chain?

– What are the tracking and tracing methods and

quality programmes that are currently in use?

– How much risk are you able

and willing to take?

– What are the quality requirements that you have to

deal with (feed safety, food safety?)

– What are the certifications, norms

and standards?

– How are these managed and controlled?

– What is the legal

context in which the liability needs to be covered?

– What are the current

financial solutions? Any more requirements? Etc.”

The above questions give a good insight into the

possible gaps and variations (non-compliance issues) regarding existing

certifications and

norms in the

sector (GMP+, ISO, HACPP, BRC). “After that, we hold interviews with the

key-stakeholders of the company (double check for possible gaps),” explains de

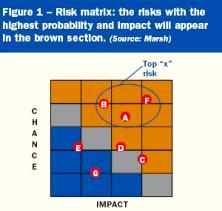

Haan. A third step in the risk inventory includes the risk matrix. The different

risks will be labelled and then plotted as to whether they are perceived as a

high or low impact (see figure 1). This makes it easier to define the

priorities and an action list. The last step is risk grading, a review for

existing processes (e.g. purchasing, quality assurance, etc.). “Having insight

into the risks and insurance covers in place, does not automatically mean that

you can lay back and relax,” de Haan continues. It remains difficult to predict

whether all potential risks are covered and if they will prove sufficient if an

incident were to occur.

More claims, contaminations and

recalls can be expected in the future, which makes adequate risk management and

(if desired) a product

contamination insurance more

important for feed companies, according to de Haan. The increased number of

claims is the result of better analytical methods (for example dioxins, PCB),

more stringent legislation (lower maximum tolerated levels in feed), increased

awareness among consumers and increased scrutiny from supermarkets. In addition,

the speed that information proliferates across the globe due to modern

communication technology ensures that any negative publicity, whether true or

not, will expound the problem. Increased knowledge on the effect of certain

toxins for human and animal health also guarantees that any problems become

front page news.

In the case of imported contaminated ingredients,

such as the wheat gluten from China (pet food) or the contaminated animal fat

(dioxin scare), the feed company that brought in the contamination always has to

recoup the losses from the previous link in the chain. “These risks, when they

result in third party damage (bodily injury or material damage) can be covered

by public and product liability insurance, but it shows that good communication

and clear agreements between companies are of utmost importance,” according to

de Haan. Does the supplier uses the same quality norms as your company? Which

agreements are put on paper in the contract? Does your supplier have adequate

insurance? These are important factors that need to be taken into account when

buying ingredients (especially) from an unknown

supplier.

Quality programmes,

hygiene and an adequate risk management are important prerequisites to produce

safe feed. However, contamination of feedstuffs may sometimes lead to recalls.

Feed companies can protect themselves against the extra costs involved in such

as recall through a special product contamination insurance. “However, insurance

is often tailormade and it largely depends on the type of business, production

volume, region, speciality of cover and values involved,” concludes de

Haan.

Join 26,000+ subscribers

Subscribe to our newsletter to stay updated about all the need-to-know content in the feed sector, three times a week.

Beheer

Beheer WP Admin

WP Admin  Bewerk bericht

Bewerk bericht